I recently completed a mission for the World Bank in South Asia, where I used the Digital Gap Assessment Framework (DGAF) to analyze how the public and private sectors can collaborate to close the digital divide. This framework offers a structured approach to identifying investment opportunities that can expand digital connectivity, while also defining the “right to play” for private capital mobilization and public investment.

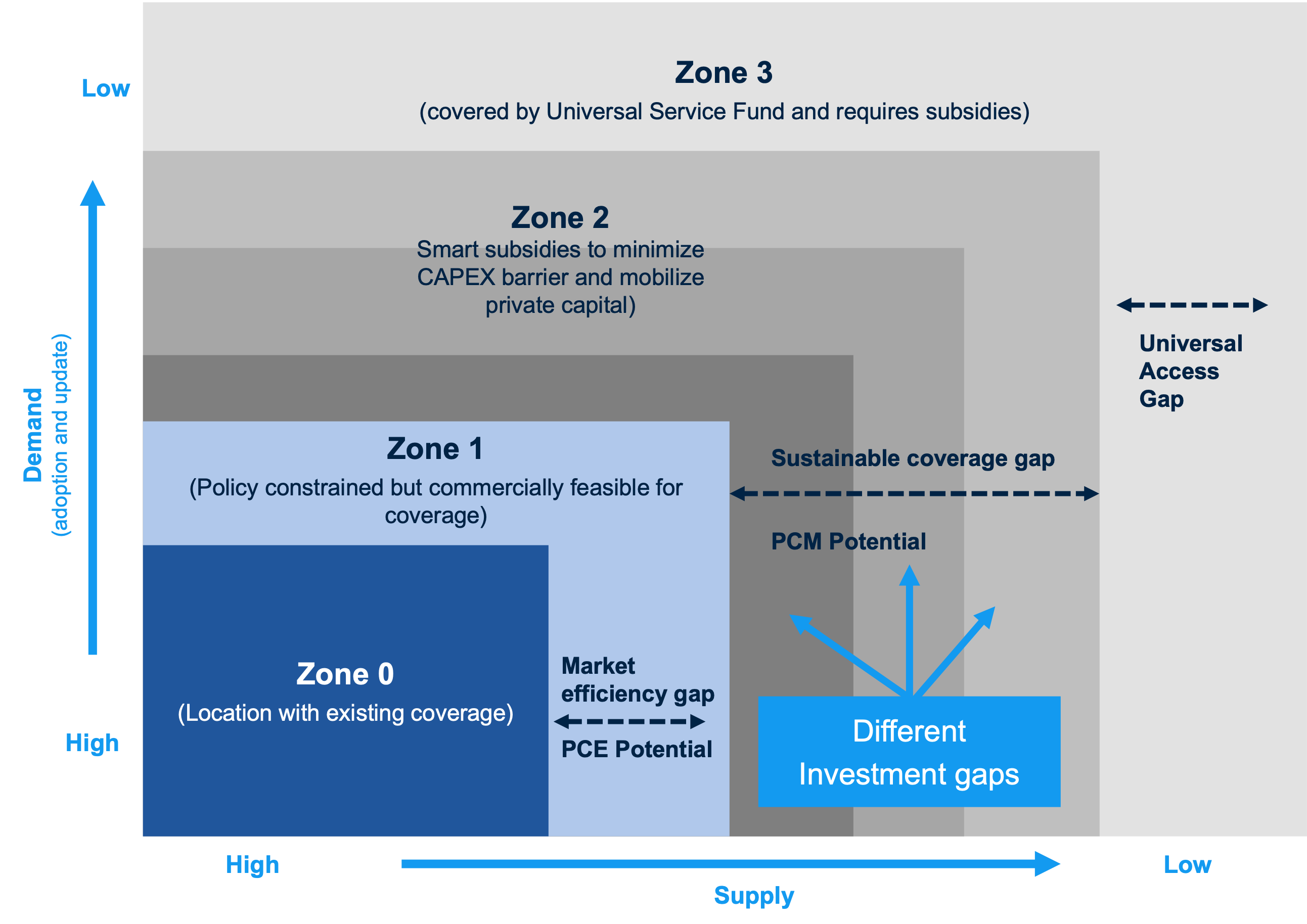

The DGAF categorizes digital access into four zones, each highlighting different challenges and opportunities for expanding broadband connectivity:

Zone 0 – Current Level of Access: These areas already have broadband services, mainly serving affluent urban households, businesses, and public institutions.

Zone 1 – Market Efficiency Gap: These areas have existing demand for broadband services, but investment is constrained by regulatory and infrastructural barriers. While private sector investment is viable, challenges such as spectrum availability, licensing restrictions, taxation policies, and regulatory uncertainty prevent deployment.

Zone 2 – Sustainable Coverage Gap: Here, broadband infrastructure could become sustainable with initial public investment. The business case for private investment exists but requires public-sector involvement to overcome high capital costs. Strategic regulatory and policy reforms are critical to ensuring long-term viability.

Zone 3 – Universal Access Gap: These are remote and rural areas where broadband deployment is economically unfeasible without continuous public subsidies. These regions depend on government support, typically through Universal Service Funds (USFs), to ensure connectivity.

Understanding these zones clarifies where the private and public sectors can play a role in expanding digital access.

Unlocking Zone 1 – The Power of Private Capital: Zone 1 represents a significant opportunity for private sector-led connectivity expansion. However, the sector is often restricted by unnecessary barriers. Private capital is available and ready to be deployed, but key constraints include:

- Regulatory restrictions—such as limitations on spectrum access.

- Complex licensing processes—which increase the cost and time of deployment.

- Taxation challenges—were regulators function as tax collectors, increasing costs for operators.

- Uncertain policy execution—creating instability for long-term investment decisions.

Solving these challenges requires regulatory and policy reforms to unlock private sector potential. For instance, allowing better spectrum allocation—such as 700MHz for greater coverage and mid-band spectrum for capacity—can immediately enhance connectivity. More importantly, a stable and predictable regulatory environment will provide the confidence needed for long-term private investment.

Supporting Zone 2 – Public-Private Collaboration for Sustainable Coverage: Zone 2 presents a complex but high-impact opportunity. The right regulatory reforms in Zone 1 are essential before public funds can be mobilized effectively. Public investment should not increase barriers but rather enable private sector expansion.

Public-private partnerships (PPPs) play a crucial role in financing infrastructure deployment in these areas. These can take different forms:

- Subsidies to reduce initial capital costs.

- Equity participation from development finance institutions.

- Loans or guarantee structures to de-risk investments.

A colleague once put it best: “All we are doing is moving the business case of private operators forward. They see the demand, but without intervention, they would only address it in a few years. Public support helps unlock that future demand today.”

Closing Zone 3 – Fully Public-Funded but Private-Sector Implemented: For Zone 3, the most remote and unviable areas, broadband deployment must be fully financed by the public sector. However, these projects should leverage the expertise of private operators for efficient implementation. Universal Service Funds (USFs)—which governments already collect—should be allocated effectively to expand connectivity in these regions.

A clear understanding of “who plays where” ensures that digital expansion efforts are both efficient and impactful:

- Zone 1 – MNOs, ISPs, and infrastructure providers should work closely with regulators to remove barriers, that will enable Local Financial Institutions and the Foreign Finance Institutions to fully invest into the private-sector.

- Zone 2 – MNOs, ISPs, and infrastructure providers, in collaboration with governments and development finance institutions, should co-finance projects through PPPs and other blended finance mechanisms.

- Zone 3 – Public sector funds should support private-sector execution, ensuring broadband deployment in unserved areas through Universal Service Fund allocations.

The path to universal broadband connectivity is clear: Empower the private sector while ensuring strategic public-sector support where needed. By addressing regulatory barriers in Zone 1, enabling PPPs in Zone 2, and efficiently deploying public funds in Zone 3, we can bridge the digital divide more effectively.

I believe the opportunity is massive and we need the right conditions for private investment to thrive and unlock digital access for all.

Leave a comment